I am jotting 5 excel quick hacks to perform Forensic Audit in Excel envoronment.

1) Identifying Duplicate Transactions using Highlight Values:

Consider the following

instance where we have a supplier name or code, supplier invoice number and the

amount. There is a chance that one might have a duplicate amount number or

duplicate invoice number for different suppliers – but what if a pair of

records have exactly the same data for all the three parameters? This is

a definite case of duplicate invoices existing:

In the above example we

have produced the column D by concatenating the data in the first three columns

and then applying the conditional formatting for duplicate values. (The

exact formula is =A2&B2&C2 in cell D2 and then dragged down, the

conditional formatting on cell D2:D13 can be applied by accessing Highlight

Values Menu from Home Tab.)

As you can see from this

screenshot, various duplicates are highlighted in the second and the third

column as well as the fourth column. We can ignore the duplicates in the

second and third column as invoice number and amount could be the same for

different suppliers – but the duplicate value in the fourth column means that

all the three parameters are the same. This points to a definite

duplicate entry that should be checked.

2) Analyzing

Round Numbered Transactions:

If a forensic accountant

is getting too many round numbers, it is time to check the accuracy of the

document or ask for further support. Too many round numbers may indicate

something fraudulent is occurring.

Excel has a built in

function called MOD () to analyze if a number is a round number or not.

The dynamics of the formula are simple – we add the following formula in the

example sheet to find if the number has to be checked for something potentially

fraudulent:

=IF(MOD(A2,100)=0,”Check”,”-“)

The formula will return a

non-zero number and the result can be presented as-is or nested into an IF()

statement to give the desired result:

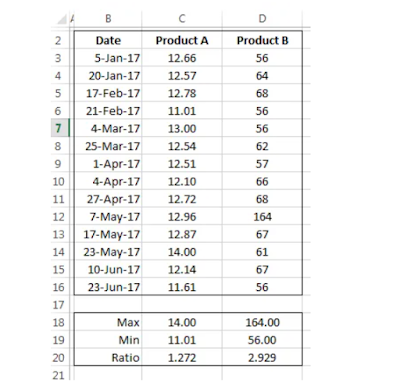

3) Above

Average Payments to Vendors or Checking the Ratio between a Maximum and

Minimum:

For a product, prices

usually fall within historical ranges. If anything goes beyond the

average, the entry can be question and should be verified. Consider data

in the following table that has price listed for two different products.

These products are bought over a period of six months and their prices vary between

a minimum of 11.01 and a maximum of 14, whereas the ratio of the max/min is

1.272. Compared to this, if we look at the second product, we find this

ratio to be 2.9 times or almost 3 times. This points to a discrepancy.

4) Gap

Detection:

This is a test that uses

a simple fact that any missing invoice (number) in the sales database can

indicate a potential problem. This test can be done for such a document

and help drive for further inquiry of the preparer.

In excel we can do this

test by first sorting the invoice number and then taking the difference of

consecutive invoices. The following screenshot how the excel sheet is

setup for this case:

In the above example, we

have setup a formula that calculate the difference between the two consecutive

invoice numbers, if it is one, then its okay and we move forward. If not,

it means that an invoice number was skipped – we can then write a conditional

formula with IF() that can give us a custom message like this:

=IF(A3-A2<>1,A3-A2-1&” – Invoice(s)

Missing”,”-“)

The above formula checks

if the difference is one, if not, we have a custom message that “n-invoices are

missing”. Otherwise, we will have a blank cell.

5) Checking

Ratio of the Highest to the Second Highest Number:

This is again a procedure

that relies on the use of finding maximum, but not just maximum but also the

second largest number in the data.

Consider the following

data for a part purchased from a supplier:

We can use build in

function MAX() and LARGE() to find the maximum and the second largest value in

the data. As we take the ratio of the data, we find it to be 10 times the

maximum number. This means that maximum for the data is much larger than the

usual average value.

Conclusion:

We cannot eliminate

mistakes or “fudging” in the financial data however we can positively try to

minimize it. We have seen five techniques that can be applied using a

standard tool like MS Excel for tracing such issues. Please download the

attached file to see it working practically.

No comments:

Post a Comment